Parsing the CCUS Supply Chain: A Series of Commercial Solutions

Drake Hernandez, Senior Fellow, Tulane Energy Law & Policy Center, Tulane University Law School and Associate Principal, Charles River Associates

Peter Davidson, Chief Executive Officer; Mary King, Vice President; Rachel Powlen, Research & Editorial Contributor, Aligned Climate Capital

Carbon capture, utilization, and storage (CCUS) is a simple concept: rather than emit carbon dioxide (CO2 or carbon), capture it and either use it as a feedstock for another process or store it permanently. While there have been false-starts in the CCUS sector, economics and policy tailwinds are pushing new-found enthusiasm for CCUS as a decarbonization solution.

Early investments in the clean energy transition have focused on electrification, renewable power production, and batteries. While these investments are foundational in the pursuit of achieving climate goals set by governments around the world, additional solutions are needed to meet climate targets for sectors that cannot be easily electrified, such as heavy industry, cement, and steel. These difficult-to-electrify sectors accounted for almost 20% of global CO2 emissions in 2021.1

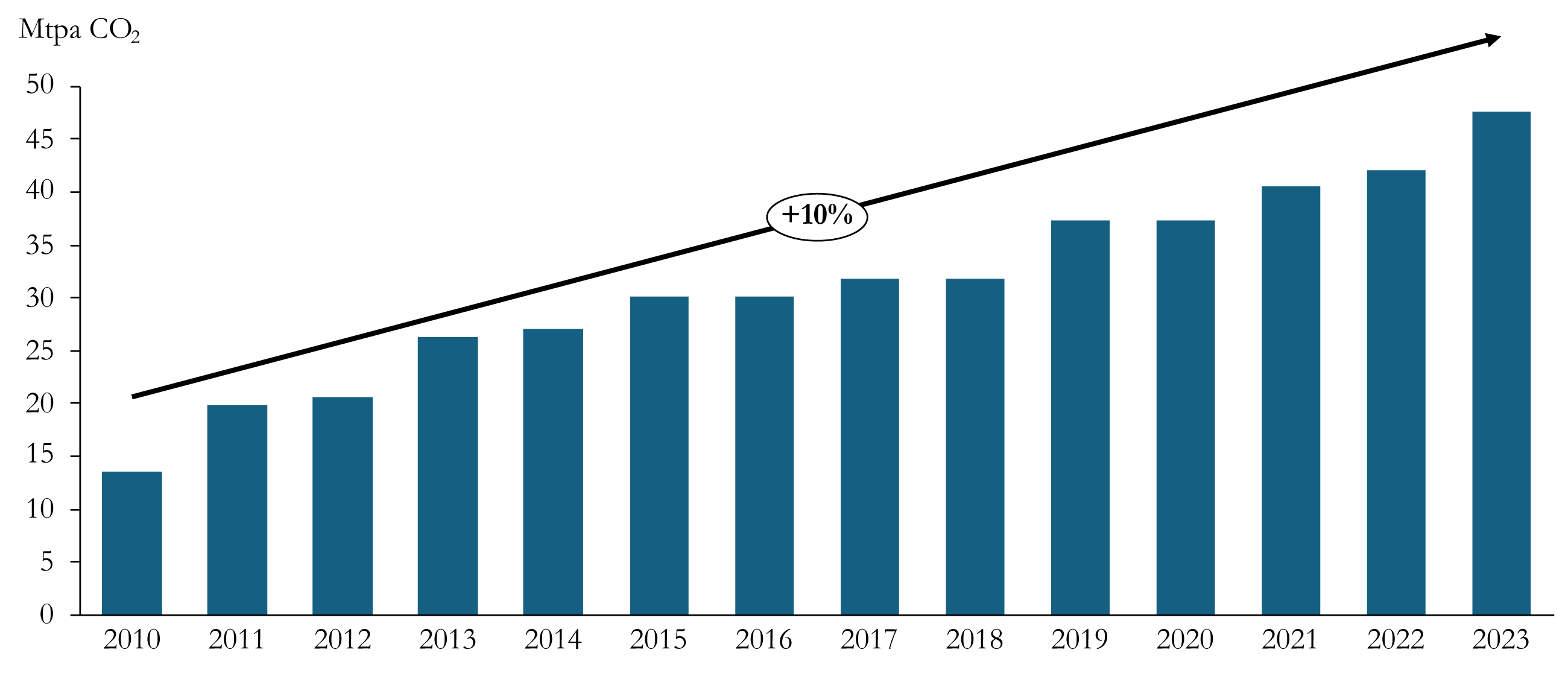

Companies are already capturing CO2 emissions and generating revenue through tax credits and CO2 off-take agreements. However, the sector is still working to create new commercial uses for CO2 to decrease the reliance on tax credits, which may face increased political pressure in the future. Even in the face of this challenge, the business case is strengthening. Importantly, every part of the point-source CCUS supply chain is commercially available today, with new projects under way and heading to market. Global CO2 capture capacity grew 10% year-on-year from 2010 through 2023, increasing from less than 15 million tons per annum (Mtpa) in 2010 to over 45 Mtpa by 2023 – as shown in Figure 1 below.

Figure 1: Globally Installed CO2 Capture Capacity2

CCUS enables a producer to transform a liability into an asset. By converting captured gases into valuable products or storing them permanently, CCUS provides a viable pathway to net-zero emissions that complements renewables and electrification. With proven technologies, scalable infrastructure, and growing financial support, CCUS is ready to contribute meaningfully to the next phase of decarbonization.

What is CCUS?

Far from being a one-size-fits-all approach, CCUS operates as a discrete supply chain with three distinct elements: capturing carbon at the source, transporting it safely, and either utilizing or storing it permanently.

Capturing Carbon at the Source

The first step in the CCUS supply chain is capturing CO2 directly from the emitting source. There are two main approaches: capturing greenhouse gases at industrial sites, referred to as point source capture, or extracting them from ambient air, a process called direct air capture (DAC).

Point source capture is proven technology and scaling rapidly. Technology can eliminate up to 95% of emissions from power plants, refineries, and industrial sites.3 This is especially useful for cement, steel, and petrochemical sectors where electrification is not yet feasible. These systems installed directly in the system, use chemical processes to extract pollutants before releasing cleaner air.

DAC, by contrast, targets legacy pollution – CO2 already in the atmosphere. Although early in its commercialization, due in large part to higher costs and energy intensity, DAC could become a key CO2 removal pathway. These systems pull in ambient air, use chemical reactions to isolate carbon dioxide, and prepare it for transport or permanent storage. The technology requires significant investment and innovation to scale, and may never reach a cost-effective price point at scale.

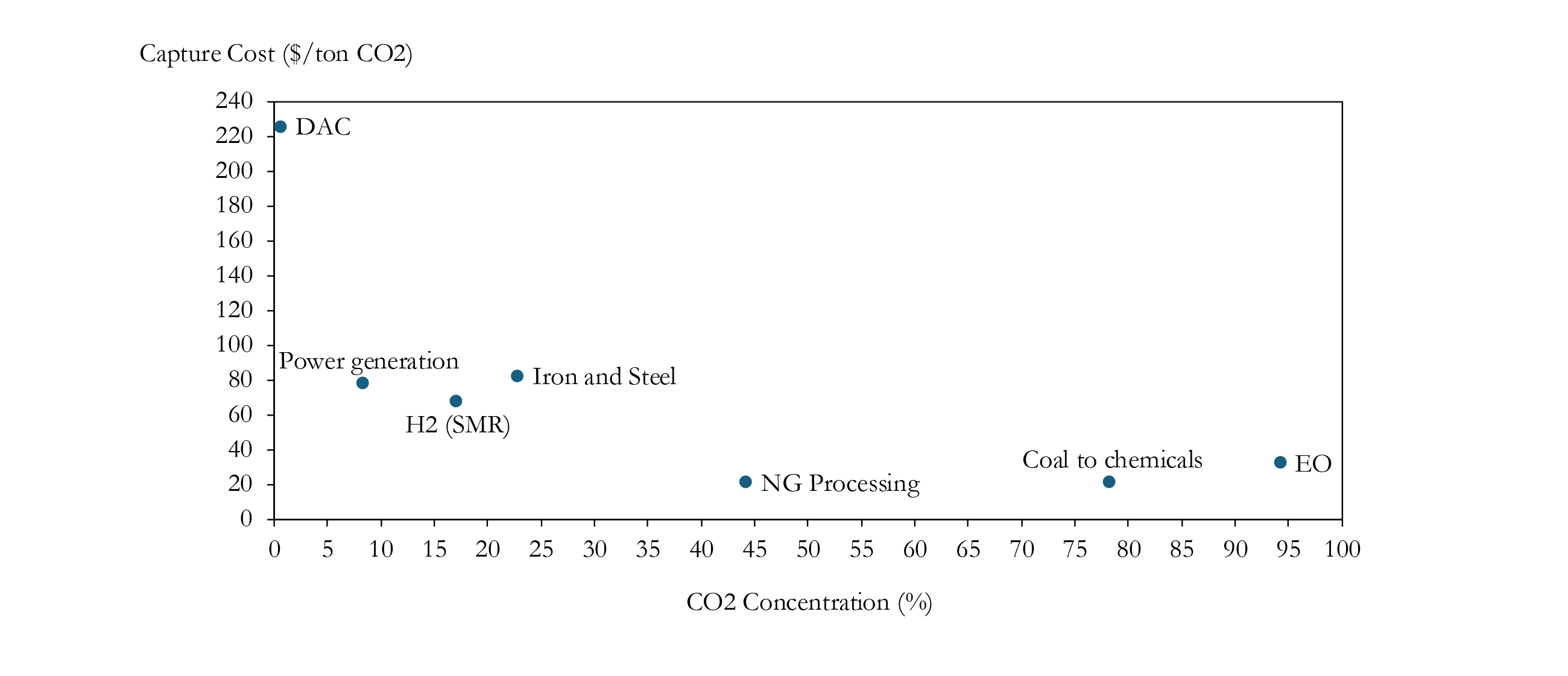

The cost of capturing CO2 is directly linked to its concentration. Point source CO2 capture, which is linked to processes with higher CO2 concentrations, typically has lower capture costs. For DAC, on the other hand, capturing CO2 is typically more expensive given the lower concentration of CO2 in the atmosphere. This is shown in Figure 2 below.

Figure 2. Cost to Capture CO2 vs. CO2 Concentration of Source4

Transporting Captured CO2

After capturing CO2, the next challenge is transporting it efficiently for use or storage. Transport is a crucial link in the chain. Captured carbon may be transported via pipelines, trucks, or even ships depending on the volume and distances involved. Pipelines are the most efficient method for large-scale, point-to-point transportation, especially in regions with existing infrastructure. On the other hand, trucks and ships offer flexibility to more remote projects.

Building out this infrastructure is no small feat. Many regions lack the pipeline networks needed to move captured carbon at scale, and in the US there have been recent regulatory challenges facing the development of new CO2 pipeline networks.5 However, the rise of CCUS hubs (networks that aggregate CO2 from multiple sources and channel it to storage or utilization sites) offer a promising way to overcome this bottleneck. These hubs could accelerate the deployment of CCUS by creating economies of scale and reducing costs.

In limited cases, recycling the CO2 onsite is a feasible solution to transportation challenges.

Utilizing and Storing CO2

The last step in the CCUS chain is determining what to do with the captured emissions. The two main options currently include transforming emissions into valuable products or storing emissions permanently.

Utilization involves converting what was once a waste stream into something useful. Companies are already turning captured gases into low-carbon concrete, synthetic fuels, and polymers. For instance, using emissions to cure concrete not only locks them away permanently but also reduces pollution from one of the world’s most carbon-intensive industries. In the case of synthetic fuels, converting captured gases into jet fuel offers a pathway to decarbonize aviation, one of the hardest sectors to electrify.

The other option is permanent storage. Geological sequestration involves injecting emissions deep underground, typically into saline aquifers or depleted oil and gas fields, where they can remain safely stored for centuries. Alternatively, captured gases may be mineralized. In Iceland, for example, emissions injected into basalt rock transform into solid minerals within just two years—a powerful demonstration of what is possible with this technology.6

Building the CCUS Ecosystem

The CCUS sector consists of many market participants, ranging from large-scale, multi-national companies to innovative startups looking to develop technologies that drive-down the cost associated with capturing and managing CO2 emissions. Other companies are deploying geotechnical expertise to develop large-scale CO2 storage facilities throughout the world.

The CO2 logistics supply chain is well established and currently in use throughout the United States. The industry has demonstrated the ability to cost-effectively move CO2 across long distances via pipeline and inject it for permanent sequestration.

The Business Case for CCUS

For industrial emitters, CCUS is no longer just a way to manage environmental obligations, but it can also provide a strategic financial opportunity. Companies that act now can leverage tax credits, carbon pricing, and commercial markets to turn emissions into a revenue-generating asset. By capitalizing on government incentives, carbon markets, and emerging CO2 utilization industries, industrial emitters can unlock new revenue streams, while meeting climate goals. Emitters can stack multiple revenue streams, including lucrative tax credits, carbon trading revenue, and CO2 off-take agreements, all while avoiding rising compliance costs.

Tax Credits and Incentives for CCUS

Governments worldwide are making CCUS more profitable than ever. In the US, the Inflation Reduction Act has nearly doubled the 45Q tax credit, offering up to $85 per ton of permanently stored CO2 or up to $180/ton for CO2 captured from a DAC facility and disposed of via geological sequestration.7 This substantial incentive is available for 12 years per project, driving financial viability for CCUS projects. For industrial emitters, this translates into immediate, bankable returns.

Governments outside the US are also competing to attract CCUS investment. Canada’s Investment Tax Credit (ITC) covers 37.5% to 60% of eligible capital costs, significantly reducing the upfront expense of capture and storage infrastructure.8 By offsetting these costs through tax relief, the ITC can help CCUS projects become cash-positive faster. Some countries, including in the EU and the UK, are developing contracts-for-difference and direct grants to ensure a predictable carbon price, further de-risking CCUS investments.9

Carbon Pricing and Compliance Market Value

Investing in CCUS not only unlocks new revenue streams but also could protect emitters from rising regulatory costs. With governments tightening emissions rules, industries face increasing penalties, carbon taxes, and compliance obligations. For high-emitting sectors, CCUS serves as a potential financial safeguard, ensuring companies stay ahead of policy shifts, while avoiding costly fines or operational restrictions.

Carbon pricing is transforming CCUS from an environmental initiative into a financial opportunity. With carbon costs rising globally, emitters are likely to look increasingly at CCUS, or other decarbonization options, or risk escalating compliance costs.

In regulated markets, every ton of CO2 carries a direct financial value. Since 2022, the price of carbon allowances under the EU Emissions Trading System (ETS) have ranged from just under €60 to over €100 per ton, raising the cost of emissions-heavy operations.10 Companies that implement CCUS can reduce their need for allowances and may even generate revenue by selling surplus credits.

Canada’s carbon tax is increasing by CAD $15 per ton annually and is expected to reach CAD $170 per ton by 2030.11 This expected increase would make the Canadian carbon tax one of the highest carbon prices in the world and positions CCUS as a critical tool for companies seeking to manage and mitigate regulatory exposure.

In tax-based systems, CCUS functions as a financial shield. Rather than directing millions toward tax payments, emitters can invest those funds in carbon capture, transforming a compliance cost into a value creation opportunity.

CO2 Off-Take Agreements and Utilization Markets

CCUS is not just about reducing emissions, it is also about turning waste into value. Captured gases are increasingly in demand across a variety of industries, offering emitters a clear path to commercialization and revenue generation.

From carbonation in food and beverage to greenhouse acceleration in agriculture, CO2 already plays a critical role as a key feedstock. Manufacturers also incorporate it into fuels, chemicals, and building materials, often through long-term, off-take agreements that secure fixed pricing.

Beyond these established uses, emerging utilization technologies are presenting new revenue streams. Captured emissions are being converted into synthetic fuels and low-carbon concrete, enabling product innovation and permanent sequestration. These markets are beginning to scale, with companies securing multi-year supply contracts. For emitters, this translates into stable revenue and stronger project financing, helping make CCUS projects commercially viable.

Conclusion

The CCUS supply chain is composed of proven technologies that are currently implemented by companies across various sectors of the economy. Around the world, supportive government policies and emerging market opportunities are creating opportunities in the CCUS sector. By tapping into multiple revenue streams, CCUS can shift from a regulatory obligation to a source of competitive advantage. With the right strategy, emitters could harness tax credits, carbon markets, and off-take agreements to deliver meaningful returns, while driving down emissions.

Charles River Associates is a leading global consulting firm that offers strategic, economic, and financial expertise to major corporations and other businesses around the world. CRA’s Energy Practice provides services to a wide range of industry clients, including utilities, ISOs, RTOs, large customers, and investors. The Energy Practice has offices in Boston, London, New York City, Salt Lake City, Toronto, and Washington, DC. Learn more at www.crai.com/energy.

Aligned Climate Capital LLC is an asset manager investing exclusively in the companies and projects driving the clean energy transition. Founded in 2019, Aligned currently manages approximately $2.1 billion of assets (as of 12/31/24). The firm’s senior leadership team brings decades of climate and clean energy experience across finance, energy markets, and government. Aligned has two primary investment strategies: the Aligned Climate Fund, which provides capital to venture-stage companies deploying and scaling established clean energy solutions, and Aligned Solar Partners, which owns and operates distributed solar, energy storage, and other clean energy projects. For more information, visit AlignedClimateCapital.com.

This paper represents the research and views of the author(s). It should not be construed as legal or investment advice. It does not necessarily represent the views of the Tulane Energy Law & Policy Center, Charles River Associates, or Aligned Climate Capital. The piece may be subject to further revision.

{kind=link}

{kind=link}